Areas of investment

We separate the size of the market into four key investment areas, also known as our ‘market systems’ – social and affordable housing, social lending, impact venture and social outcomes contracts.

-

Find out more about our market systems approach

Learn more

Case study

Savills IM Simply Affordable Homes Fund

Fund aiming to increase the availability of affordable homes in the UK.

The challenge

The UK faces a significant shortage of affordable homes with an estimated £250 billion by 2031 of investment needed to address this shortfall.

Our approach

Better Society Capital invests into best-in-class social property funds aiming to attract institutional capital at scale that will unlock new, affordable housing supply.

The Fund

Will deliver a combination of new, affordable homes and acquire existing stock from housing associations and registered providers, thereby freeing up capital for these organisations to develop more homes and reinvest in existing homes. The fund will deliver affordable and social rent, as well as shared ownership homes, via an open-ended fund structure.

The Fund’s assets will be owned and managed by the Fund’s Registered Provider, Simply Affordable Homes RP Limited. The Fund operates under enhanced impact frameworks and a sustainable investment strategy.

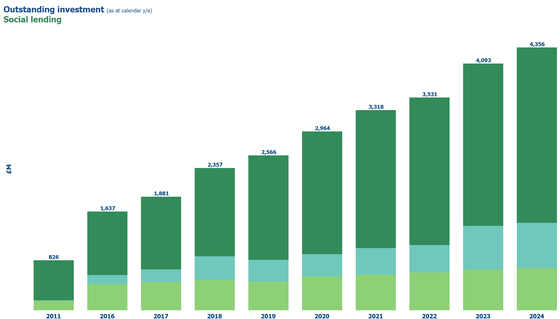

Social lending

Social lending accounts for 39% of the overall 2024 market, down from 41% in 2023.

Outstanding investment in social lending has increased by 6% since 2023 to ~£4.4 billion in 2024 (£4.1 bn in 2022).

Deal flow is slightly down from £956m to £922m (a drop of about 4%); this is primarily due to a large drop in deal flow in bonds from £256m in 2023 to £35m in 2024, which is itself mostly due to a drop-off in deal flow reported by Allia; banks see an increase in deal flow from £502 to £690m and non-banks have a small increase from £178m to £196m.

Outstanding investment across all 3 areas of social lending have increased since 2023:

- Bank Lending refers to loans made to charities and social enterprises by dedicated social banks – this area has shown an increase of 8% in size from £2.7bn to £2.9bn in 2024.

- Non-bank lending refers to debt finance taken on by charities and social enterprises to provide working capital and growth finance. This asset class also includes investments made into community shares and crowdfunding platforms – this area has shown an increase of 3% from £680m to £700m in 2024.

- Charity Bonds refer to tradable loans that offer large scale unsecured finance with fewer restrictions than bank finance – this area has shown an increase of 4% from £719m to £750m in 2024.

- Community Investment Enterprise Fund provides debt finance to CDFIs with the capital they need to meet the demands of small businesses.

- CORE – Community owned renewable energy puts renewable energy into community hands to help make places better for people, whilst accelerating the transition to net zero.

- Energy Resilience Fund is aimed at supporting community and social enterprises to reduce energy usage, stabilise energy costs and contribute to long-term Net Zero goals.

Case study

Community Investment Enterprise Fund

Providing debt finance to Community Development Finance Institutions (CDFIs).

The challenge

Small businesses are essential to local communities, creating jobs and bolstering economic activity, however many are unable to access mainstream finance. While they can access finance from socially motivated lenders such as Community Development Finance Institutions (CDFIs), the CDFIs themselves face barriers to achieving long-term sustainability and securing capital at scale to meet the demand of small businesses.

Our approach

We established the Community Investment Enterprise Fund (CIEF) in 2018 to provide CDFIs with the capital they need to meet demand, and to help increase understanding of the financial and social impact of CDFI lending to attract other investors to achieve growth and long-term stability.

The Fund

The fund provides capital for three CDFIs based in Wolverhampton, Doncaster, and Bradford, to help them lend to small businesses operating within surrounding areas.

The first phase of the fund saw the deployment of £72m by four CDFIs, to meet the needs of more than 960 businesses, with co-investment from Triodos and Unity Trust Bank. In April 2020, the Community Enterprise Investment Facility was adapted as part of Better Society Capital’s response to the coronavirus pandemic to ensure it could access the Government-based Coronavirus Business Interruption Loan Scheme, meaning CDFI’s could provide smaller, emergency loans on a no fee, no interest basis for 12 months for underserved businesses affected by Covid-19.

In 2024, the second phase of the fund begun, with co-investment from Lloyds. Lloyds has become the first mainstream lender to support the CDFI sector, underlining its commitment to investing in sustainable business and regional development including within disadvantaged areas of the UK. The fund continues to be managed by Social Investment Scotland.

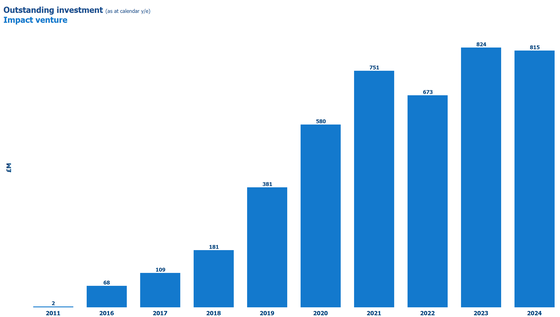

Impact venture

Impact venture currently accounts for 7% of the overall 2024 market.

Outstanding investment in impact venture has decreased by 1% since to £815m (£824m in 2023).

Deal flow is estimated at £121 million, broadly in line with 2023 levels. According to Dealroom’s State of Impact 2025 report, global impact venture funding is expected to reach $33 billion in 2025, a 24% decline from 2024, marking the sharpest slowdown since 2019. This decline reflects a broader pullback in climate-focussed investment, which had expanded significantly between 2020 and 2022. Despite this cooling, the long-term trajectory of impact investing remains positive, with the total value of impact-oriented companies growing 28-fold over the past decade to $3.6 trillion, signalling a market that is recalibrating rather than contracting.

Within the UK, investment continues to focus on health and financial inclusion, consistent with previous years. These areas attract significant capital from mission-driven investors seeking to address social challenges such as improving wellbeing, access to services, and economic resilience for underserved communities. Interest in impact investing continues to build, reflected in ImpactVC’s expanding global network, which has grown to over 750 member firms since its launch in 2023.

We view our figure as a conservative estimate of overall market activity, given the limited visibility into venture investments that intentionally pursue social impact and the fast-evolving nature of the market.

- Ascension Fund III | Better Society Capital invests in tech businesses that tackle the cost-of-living crisis through increased income opportunities, access to healthcare and affordability of essential goods.

- EKA invests in businesses delivering affordable and preventative health interventions and socially and environmentally sustainable supply chains.

- Meridian Health Ventures I invests in digital health, enterprise healthcare, and MedTech companies providing solutions where there is a compelling case that the company can scale within the NHS.

Case study

Ascension Fund III

Ascension III is a pre-seed/seed stage venture fund aiming to reduce social inequality by investing in tech businesses that tackle the Cost of Living Crisis through 3 key themes: increase income opportunities; decrease costs of essential goods and improve access to healthcare.

The challenge

Income levels are not keeping up with the rising cost of living due to: stagnant wages, reduced social mobility and the rise of the gig economy, with volatile revenues and an economic system not built to optimise them. In addition, while lower-income households are disproportionately affected by the Poverty Premium, the Cost of Living Crisis has driven up the cost of essential goods, impacting a broader segment of the population. This has further exacerbated the negative impact of the pandemic on health outcomes. The pandemic disproportionately hit lower income or underrepresented communities, which affects the ability to earn, increases average spending and in turn creates structural disadvantages in a rising cost environment.

The Fund

Ascension III is a pre-seed/seed stage venture fund aiming to reduce social inequality by investing in tech businesses that tackle the Cost of Living Crisis through 3 key themes: increase income opportunities; decrease costs of essential goods and improve access to healthcare.

One example of their recent investments is Juniver which is a neuroscience-based programme created by eating disorder clinical experts and a team with experience recovering from eating disorders. Juniver is aiming to transform the eating disorder market through a first-of-its-kind digital solution with an AI-powered assistant for on demand help through urges, personalised insights from health data, peer support and telemedicine care.

User Voice

All of Ascension III's investment decisions are supported by a lived experience panel embedding user voice across the investment process. The findings from the user panel showed a strong interest in using the AI-driven Juni to curb binges, with 81% of respondents saying they would use the app for managing their eating disorder.

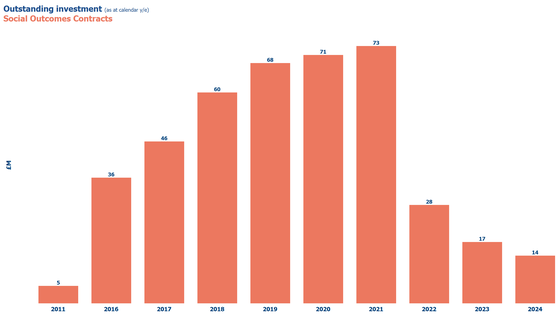

Social outcomes contracts

Currently accounts for less than 1% of the overall 2024 market.

Outstanding investment in SOCs has reduced to £13.5m in 2024 (£17m in 2023)

While the slight reduction since the 2023 market sizing reflects the natural conclusion of several contracts, there has been considerable progress and renewed momentum across the market that is set to drive future growth.

The UK Government’s recent announcement of the Better Futures Fund, a £500 million commitment to outcomes-based commissioning over the next decade, marks a major step forward. Although still in the design phase, the Fund is expected to expand the scale and reach of the SOCs market in the coming years.

The establishment of the Office for the Impact Economy will also serve as an important catalyst for collaboration and investment. By acting as a central hub for impact investors, philanthropists, and purpose-driven organisations, the Office will help channel growing interest and capital into projects that deliver measurable social impact across the UK.

- Bridges Social Outcomes Funds | Better Society Capital is dedicated to supporting social enterprises and charities with capital they need to deliver Government-commissioned outcomes contracts.

Case study

Bridges Social Outcomes Funds

Funds dedicated to supporting Government-commissioned outcomes contracts.

The challenge

Public sector commissioners are looking for more flexible ways to drive innovation and improve lives in key policy areas such as homelessness and youth unemployment by using outcomes-based contracts. But social enterprises and charities often lacked the upfront working capital to deliver these contracts.

Our approach

We issued a call to establish a specialist fund that could provide social enterprises and charities with the capital and support they need to deliver outcomes-based contracts. As the first fund of its type in the world, this would also help catalyse the broader market. There have since been over 40 of these projects commissioned by Government in the UK.

The Fund

The original Bridges Social Outcomes Fund was designed to offer mission-driven providers with the working capital and management support they need to deliver these contracts, where payment is dependent on measurable improvements in the lives of service users.

This fund was the first of its kind; so as well as delivering demonstrable social impact, the intention was to develop a replicable fund model that allowed socially-motivated investors to support these contracts.

Its successor fund – Bridges Social Outcomes Fund II – is building on these learnings to support larger projects and help this market succeed on a bigger scale.

Find out more about Bridges Outcomes Partnerships, a social enterprise that supports impact-driven delivery organisations to develop and deliver outcomes-based contracts.

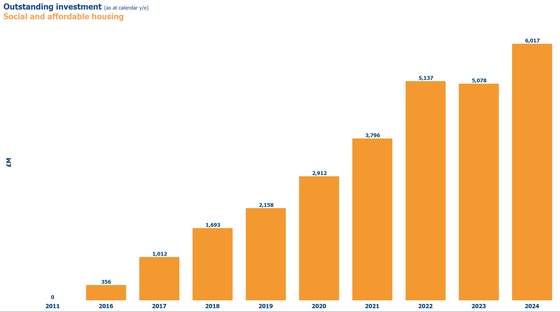

Social and affordable housing

Social and affordable housing funds account for 54% of the overall 2024 market size.

Outstanding investment in social and affordable housing has increased by 18% this year to £6bn. Deal flow has increased from £861m in 2023 to £1090m in 2024 (an increase of about 27%), and a reversal of the drop seen from 2022 to 2023.

The increase in overall market size corresponds with increased Pension Fund investment activity in social and affordable housing, particularly the Local Government Pension Schemes (LGPS) who are seeking resilient returns alongside tangible impact.

The most significant contributor to this is M&G who have reported an increase in valuation of £336m.