Areas of investment

We separate the size of the market into four key investment areas, also known as our ‘market systems’ – Social and affordable housing, Social lending, Impact venture and Social outcomes contracts. Find out more about our market systems approach.

-

Find out more about our market systems approach

Learn more

Case study

Notting Hill Genesis

Notting Hill Genesis, as one of the largest housing associations in the country, is dedicated to addressing homelessness and the wider housing crisis by providing quality affordable housing.

Challenge

The homelessness crisis in London continues to spiral. According to London Council’s recent estimate, 170,000 people in the city are homeless and residing in temporary accommodation - one in 50 of the capital's entire population. On average there is at least one homeless child in every London classroom. Despite the boroughs' efforts to assist homeless households; the shortage of available properties, especially in the lower market segment, has intensified that challenge. Research by Savills and the LSE indicates a 41% decrease in listings of PRS (Private Rented Sector) properties and a 20% increase in rents since the onset of the Covid-19 pandemic. In 2022-23, only 2.3% of PRS housing was deemed affordable for low-income households relying on Local Housing Allowance to cover their rent.

Approach

Notting Hill Genesis, as one of the largest housing associations in the country, is dedicated to addressing homelessness and the wider housing crisis by providing quality affordable housing. With more than 60,000 homes in its portfolio across London and the South-East, it offers a variety of tenures, including social, affordable and private rent; leasehold; key worker housing; temporary housing and shared ownership. It operates with a resident-centric philosophy, emphasising three core priorities: "better connections," involving actively listening to residents' concerns and engaging with their needs; "better homes," striving to ensure safe and comfortable living regardless of tenure; and "better places," managing estates in a holistic manner that enhances the sense of community.

In 2023 it partnered with Resonance’s National Homelessness Property Fund 2, through which it will manage almost 600 properties aimed at supporting families in the highest need by providing vital temporary housing to those who would otherwise have nowhere to go.

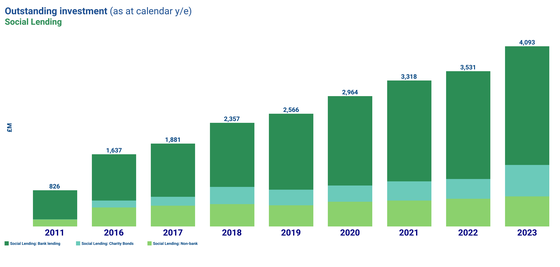

Social lending

Social lending accounts for 41% of the overall 2023 market, up from 37% in 2022.

Outstanding investment in social lending has increased by 16% since 2022 to ~£4.1 billion in 2023 (£3.5 bn in 2022).

Outstanding investment across all 3 areas of social lending have increased since 2022:

- Bank Lending refers to loans made to charities and social enterprises by dedicated social banks – this area has shown an increase of 10% in size from £2.5bn to £2.7bn in 2023.

- Non-bank lending refers to debt finance taken on by charities and social enterprises to provide working capital and growth finance. This asset class also includes investments made into community shares and crowdfunding platforms – this area has shown an increase 9% from £627m to £680m in 2023.

- Charity Bonds refer to tradable loans that offer large scale unsecured finance with fewer restrictions than bank finance – this area has shown an increase of 58% from £454m to £719m in 2023

Increases in the market size across social lending are driven by small increases in underlying value of investments from 2022, new inclusions of charitable bonds into housing associations, notably £200m deal flow in 2023 relating to the Scottish Charitable Bond Programme, and 2 new contributors (Ceniarth and People's Postcode Lottery).

An increase in outstanding value across each of the three areas of social lending, especially in non-bank lending, highlights the ongoing resilience from charities and social enterprises. However, the market continues to demonstrate an increased need for blended capital to secure investment across the UK to both broaden geographic reach and attract more private capital alongside public and catalytic investment.

Find out more on our approach to Blended Finance.

- CORE – Community owned renewable energy puts renewable energy into community hands to help make places better for people, whilst accelerating the transition to net zero.

- Energy Resilience Fund is aimed at supporting community and social enterprises to reduce energy usage, stabilise energy costs and contribute to long-term Net Zero goals.

- Social Impact Debt Fund IV provides unitranche funding of up to £4m to impactful enterprises with balance sheets to support secured debt.

Our enterprise level data lists the transactions made between fund managers and other intermediaries and social purpose organisations from 2002 to 2023. The data identifies the types of organisations using social investment and enables us to understand more about their outcome areas, end-users, business models and geographies.

The latest data (as of December 2023) now captures over 7,000 commitments totalling £3.6 billion of investment into social purpose organisations. The data includes approximately £0.5billion of new commitments made in 2023 into over 700 organisations.

You can find out more about the composition of the market here. This is not a complete set of all social investment activity in the UK, but a voluntary collaborative effort from those across the sector. We are grateful to our partners for their contribution, and we encourage other investors to share their data, demonstrating the impact that social investment is having to front line organisations. To access the open data set and find out more, please get in touch.

Case study

The Children’s Trust

The Children’s Trust provides intensive rehabilitation for children with acquired brain injuries and services for children with neurosdisability.

Challenge

Each year, 40,000 children in the UK experience an acquired brain injury. This can have a catastrophic effect on a child’s life, with many children losing the ability to walk, talk and feed themselves. Early rehabilitation is crucial, but very few organisations in the UK are fully equipped to offer the level of intensive therapy and care that is required.

Approach

The Children’s Trust provides intensive rehabilitation for children with acquired brain injuries and services for children with neurodisability, It is the only national inpatient facility for neurorehabilitation for children of its kind in the UK. Director of Therapies and Education, Melanie Burrough, explains, “When a child has an acquired brain injury, it is important that rehabilitation and therapy is provided as early as possible. Once the child is medically stable, they need rehabilitation to happen as soon as possible. That gives them the best chance of regaining, relearning and adapting skills such as walking, talking, eating, getting dressed and playing.” Rehabilitation is based on individualised child and family goals to support recovery, education and participation in everyday life. Intensive rehabilitation involves a large specialist team and offers high intensity therapy over the duration of placement, which could be up to 25 hours per week.

The Children's Trust also offers community rehabilitation, short breaks for children with complex needs and step-down packages of care. The Children’s Trust School is a non-maintained school provision, with onsite residential children’s homes supporting up to 44 children, predominantly with profound and multiple learning disabilities and complex health needs.

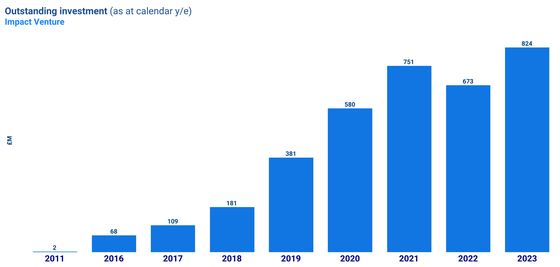

Impact venture

Impact venture currently accounts for 8% of the overall 2023 market.

Outstanding investment in impact venture has increased by 22% since 2022 at £824m (£673m in 2022).

This year we have included 5 new managers and funds from our Impact VC community which meet our impact intent definition, which has driven much of the growth. Removing the 5 additional new funds, the market growth would be up 3% from 2022.

The market growth from existing funds and contributors reflects a challenging fundraising year however our estimate reflects an increase in venture funds tilting towards impact with the addition of the new contributors. This aligns with broader market commentary around a global slowdown in VC funding as referenced by Dealroom alongside evidence of increased interest in impact with the launch of Impact VC in 2023, a global community of VCs interested in impact, that has grown to >600 firms with >£50bn AUM collectively.

We believe our figure is an estimate of the lower bound of the market, given the challenges in visibility into venture investments that are intentional about the impact they seek and the pace of the market.

- Eka Ventures Fund invests in consumer technology companies building a healthier, more sustainable and inclusive economy.

- Fair by Design Fund invests debt and equity in early-stage businesses aiming to eliminate the poverty premium in the UK.

Case study

Flok Health

Flok Health is the UK’s first AI-operated physiotherapy clinic, providing NHS patients with immediate access to personalised care, at population scale.

Challenge

The NHS remains a chronically understaffed and underfunded public service, leading to increased wait times, particularly for musculoskeletal (MSK) issues such as back, neck, and knee pain, which account for up to 30% of GP consultations in England. NHS data shows that waiting lists for MSK treatments have grown by 27% since January last year.

Approach

Flok is the UK’s first autonomous physiotherapy clinic, providing same-day access to care for NHS patients. Individuals seeking physiotherapy for issues such as back pain can be referred to the platform through a community or primary care setting, such as their GP. They also have the option to self-refer directly into the service.

An initial video assessment with an AI physiotherapist is conducted to evaluate their symptoms. Once approved for treatment, patients can schedule weekly video appointments with their AI physio, who prescribes exercises and pain management techniques, monitors symptoms, and adjusts treatments accordingly. A dedicated clinical team of physiotherapists and doctors oversees patients' recovery remotely, stepping in when additional information is needed or to further optimise the treatment plan.

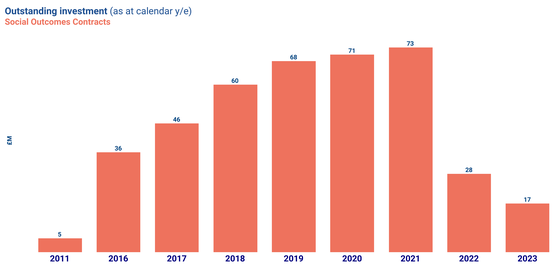

Social outcomes contracts

Currently accounts for less than 1% of the overall 2023 market.

Outstanding investment in SOCs has reduced to £17m in 2023 (£28m in 2022).

This reduction is due to contracts ending in late 2022 and 2023.

BSC, alongside others, continue to call upon the Government to reallocate budgets to these multi-year outcomes funds. Learnings over the last 13 years have demonstrated the value of social outcomes contracts, enabling Government to spend smarter whilst tackling complex social issues.

- Bridges Social Outcomes Funds dedicated to supporting Government-commissioned outcomes contracts.

Case study

Thrive Social Prescribing

Thrive Social Prescribing, or Thrive Northeast Lincolnshire (Thrive.NEL), supports people aged 18-75 with at least one of eleven long-term health conditions (including but not limited to asthma, chronic heart disease, diabetes and hypertension) to create sustainable lifestyle changes and improved self-care habits.

Challenge

It is well-evidenced that 80-90% of health outcomes such as quality and length of life are influenced by socioeconomic and environmental factors. However, traditional medical care continues to be the most prevalent solution for people with long-term health conditions like diabetes or chronic obstructive pulmonary disease (COPD). Approximately 20% of the UK population is estimated to live with long-term health conditions, the treatment for which accounts for nearly 80% of NHS expenditure.

Approach

Thrive.NEL is an outcomes-based partnership in Northeast Lincolnshire focused on achieving shared goals – in this case, the improved health and wellbeing of individuals living with long-term health conditions (LTCs).

The programme connects participating local residents to social activities like gardening, walking clubs and volunteering, while also offering practical support through social welfare, money management, and dietary advice. This approach is known as ‘social prescribing’ and offers an alternative to traditional medical care, leveraging community initiatives and services to enhance long-term health and independence.

The delivery organisation, Centre4, manages a team of Link Workers who engage with individuals referred to the programme. Together, with participants, they formulate an action plan to empower them to improve their lifestyle habits, engage in activities, and build new social connections. This holistic approach fosters greater community engagement and encourages participants to adopt a more positive, resilient attitude towards challenges, leading to an overall improvement in their wellbeing and lifestyle.

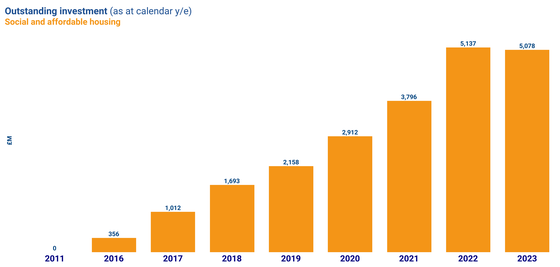

Social and affordable housing

Social and affordable housing funds account for 51% of the overall 2023 market.

Outstanding investment in social and affordable housing has remained relatively stable since 2022 at £5.1bn.

Although outstanding investment is stable compared to 2022, the value of the funds we have included in both years have increased by 11% and deal flow has increased by 3%. This shows an overall increase in the value of investments and new deployment year on year has been relatively stable. The reason for stable growth overall is due to a consolidation of market participants that meet our impact intent criteria.

We have also included one new fund this year, Henley Secure Income Property Fund, which meets our impact intent definition as set out above: (link to definition set out here in methodology and definitions section). Figures indicate that during the macroeconomic turbulence of recent years, social and affordable housing proved more resilient than other real estate sectors.