Welcome to our impact report

The UK faces entrenched social issues that require targeted investment at scale.

Across the country people are struggling with the cost-of-living crisis and rising inflation. Housing is less affordable, the NHS is struggling to cope with huge demand, and as we strive to meet net zero our most vulnerable communities are at risk of being left behind. More than 100,000 households including 130,000 children live in temporary accommodation, the highest figure since records began.

Tackling the chronic shortage of social and affordable housing alone requires an estimated £16.9bn every year for the next ten years. To effectively respond to these social challenges at scale, the crowding in of targeted private investment, seeking impact alongside financial returns, is needed.

This is our mission at BSC – to grow the amount of money invested in tackling social issues and inequalities in the UK. We aim to do so by investing our own capital, and helping to build a diverse and inclusive market that enables more social impact investment. We seek to maximise the positive impact on people, by scaling the flow of capital and availability of appropriate financial products to a range of impact-led business models, acknowledging that it is not our role to meet the financing needs of all social sector organisations.

Our Impact Report sets out how we live up to this mission and what we are learning at two levels of impact. Firstly, at the level of directly helping build the social impact investing market in the UK, and secondly and subsequently, at the level of creating positive impact in people’s lives in the UK, through the enterprises and charities that receive investment from the fund managers and intermediaries that we directly support.

Our interpretation of investor contribution, versus impact on people: Our approach to impact, differentiates between the impact on people that enterprises and charities help create, and the contributions BSC is making to build the market and enable such impact. We consider not only our capital as part of our “investor contribution”, but all our market infrastructure building activities that intend to increase the flow of capital to impact-led organisations and support positive impact on people.

We are sharing this report as an effort to be clearer and more transparent around our market-building goals and strategies, the progress we are making against them, and what we are learning along the way. In doing so, we are aware of the shortcomings of this report, when considering emerging good impact reporting practice. We are equally aware though that reporting practice for the type of systemic changes that BSC seeks to affect, remains very much in its infancy. We are excited and committed to play an active role alongside others in further defining this important field of practice.

The report also addresses our work on Equity, Diversity and Inclusion (EDI), both in terms of our role as investor and market-builder, and within BSC itself. In this year’s report we place particular focus on improving transparency on diversity data within BSC and our portfolio.

Finally, we would like to thank all our partners that share our passion for impact and building a market where more capital is invested for addressing pressing social issues in the UK. It is ultimately the many enterprises and charities across the UK that turn capital into meaningful positive changes in people’s lives across the UK.

Report highlights

We continue to make significant progress in building a social impact investing market in the UK that delivers impact across several pressing social issues, with a focus on vulnerable people across the UK.

We have seen consistent market growth over the years, despite a range of external challenges faced.

Such impact-led organisations are addressing pressing social issues, such as housing, employment, training, and education, health, and financial inclusion – and reaching into UK’s most disadvantaged areas.

Read more about our impact

We are creating immediate solutions to the cost-of-living crisis through the establishment of the Energy Resilience Fund alongside building for the long term through our investments in blended capital, debt funds and social banks.

Read more about our work in social lending

We see continued appetite for the sector from Local Government Pension Schemes targeting levelling up investments, despite a changing macroeconomic environment.

Read more about our work in social property

In impact venture, we seek to influence impact practice and build community. We launched the VC community platform, Impact VC, which now features more than 750 people and our VC Impact Playbook has been downloaded over 1,000 times.

Read more about our work in impact venture

In Social Outcome Contracts (SOCs), we see increasing interest and support among key stakeholders such as Treasury and the NHS Confederation for SOCs, which to date have reached 55,000 vulnerable people across the UK.

Read more about our work in Social Outcomes Contracts

Representing the diversity in the social investment market is key to success. Our portfolio outperforms industry (private equity and venture capital) averages on diverse representation; but significantly more work is needed by us and our partners to live up to our aspirations of building a diverse and inclusive social impact investing market in the UK.

Read more about our ESG and EDI initiatives

Our impact

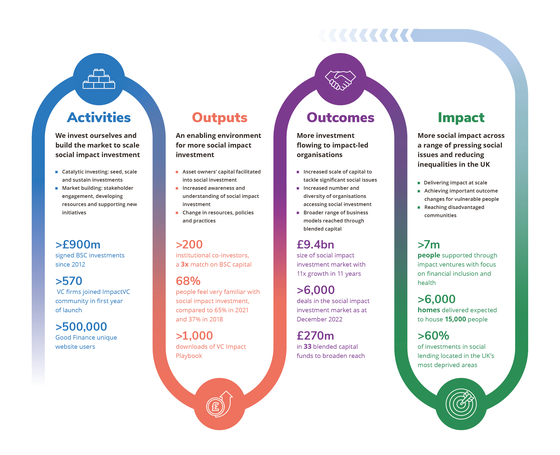

We intend to grow the amount of money invested in tackling social issues and inequalities in the UK. Our Theory of Change illustrates how we intend to achieve such change, by building an enabling environment for more investment to flow to impact-led organisations

We are aware that building a market is anything but linear. Markets are complex, social systems are often hard to predict and constantly evolve and adapt. Nevertheless, given the increasing prominence of the Theory of Change model in impact investing in the UK, and existing levels of familiarity across different stakeholders, we use it to illustrate how our activities are meant to contribute to positive impact in the UK.

Case study

Influencing policy – mobilising additional dormant account funding

We work collaboratively with partners across the sector to make the case for social impact investment to government.

Barrier to market growth

Government has powerful tools to help shape the social impact investing market. Policy – such as tax reliefs and regulation – or public spending that can be delivered in a way to unlock investment. But awareness, understanding and experience among policy-makers is low on how to use these key mechanisms to grow investment and harness more private capital for public good.

Activities

Our approach is to work in collaboration with other key organisations in the sector, providing a consistent voice to inform and support government at all levels from political decision-makers to technical policy developers. We form coalitions where appropriate, to influence and educate on key issues such as the allocation of dormant assets, or the creation of a dedicated tax relief to encourage social investment. We also work more directly with policy-makers looking to increase the impact of specific departmental spend, by leveraging in capital alongside it.

Outputs, outcomes and impact

Examples of the changes resulting from this approach include the government’s decision in 2023 to allocate £87.5 million from the next tranche of dormant assets towards the objective of broadening the reach of social investment to currently underserved enterprises and communities. The Government’s decision followed a co-ordinated campaign and representation from BSC and the sector.

Another recent example, showing how our work can lead to actual outcomes, includes the decision by HM Treasury during the pandemic to extend the CBILS guarantee scheme to non-profit organisations, including charities, after evidence from BSC that we would then be able to provide emergency lending support through our partner funds, helping hundreds of organisations.

Illustrating how our work can lead all the way to impact, working with government departments has increased the amount of capital invested in public priorities. For example, a £25 million investment from the Department for Levelling Up, Housing and Communities (DLUHC) leveraged in an additional £123 million from other investors, trebling the number of homes provided to 800 for individuals and families who were homeless or stuck in temporary accommodation.

BSC's Theory of Change

We have been articulating our market-building and impact intentions along a Theory of Change since 2015. While the complexity of our work and understanding of the market have increased since then, we have tried to keep simplifying our Theory of Change, to use it as an internal and external engagement and communication tool.

Our Theory of Change illustrates how our activities – our catalytic investing and market-building work – are expected to help address important barriers across key stakeholders (investors, fund managers, enterprises, policy-makers etc) and market infrastructure, and build an enabling environment that unlocks more capital flow from asset owners to impact led-organisations with a range of business models and different capital needs. As a result, we expect more impact-led organisations to be able to address pressing social issues and maximise their social impact in the UK, with a focus on disadvantaged communities.

Find below a more detailed description of our activities, market level-outputs and outcomes, and impact on people. We are aware that key changes in our theory of change result from a broad range of interconnected, influencing factors, well beyond our own interventions strategies. Evidencing market-level changes in our theory of change is difficult and limited in this report. It is even more challenging attributing such market-level changes to any specific intervention from us or anyone else. The very nature of how systems change in non-linear ways, makes such attribution difficult.

BSC activities

What we do broadly falls into two categories:

1. Catalytic investing

We invest across a broad range of private market asset classes in fund managers, social banks and other intermediaries.

- Seed investments – to develop, test and build track record of new and innovative impactful business models, investment products and fund managers. For example, the Fair by Design fund.

- Scaling investments – to scale proven business models, investment products and fund managers, and crowd in new capital. For example, National Homelessness Property fund 2.

- Sustain investments – to support impactful business models, products and managers that require subsidy on an ongoing basis. For example, the Growth Fund.

2. Market-building

We deploy a range of market-building strategies to influence the mindsets, knowledge and behaviours of existing market stakeholders, including fund managers, investors, enterprises and policy-makers.

- Engagement and influencing of fund manager, investor, enterprise and public policy – all to create awareness, build knowledge and capacity, and ultimately shift behaviours.

- Development of impact investing standards, tools and resources.

- Development (support) of new organisations, initiatives and communities (of practice).

Market-level outputs and outcomes

Outputs

Our activities help build an enabling environment for more social impact investment, by addressing some of the required changes across key stakeholders and market infrastructure:

- More direct BSC and co-investment in impact managers and products.

- More impact managers and products with appropriate scale and track record available that serve the needs of investors and enterprises.

- More and diverse impact-led organisations considering investment.

- Changes in awareness, knowledge and mental models across investors, fund managers, enterprises and policy-makers.

- Changes in availability of impact management tools, standards and resources.

- Changes in practices and policies among key stakeholders.

- Changes in the institutional landscape of the market (ie new organisations, communities).

Outcomes

We expect that these changes will ultimately lead to more investment flowing to an increasing number and diverse set of social enterprises, charities and other impact-led organisations with impactful business models and different capital needs.

Impact

As a result of taking on social investment, charities, social enterprises and other impact-led organisations are able to grow or sustain their impact across important social issue areas and needs across the UK, with a focus on vulnerable people and more disadvantaged areas and communities.

Some of the enterprise models we support, such as those using digital delivery, are able to achieve significant scale of people reached – others, such as housing models, focus on delivering depth of impact for a smaller group of vulnerable people. For all our investments we prioritise reaching the UK’s most deprived areas and communities.

Case study

Good Finance - enabling charities and social enterprises to navigate social investment

A collaborative project to help improve access to information on social impact investment for charities and social enterprises.

Barrier to market growth

The complexity of social investment can be challenging to navigate for charities and social enterprises. Many time- and resource-strapped organisations find it hard to understand whether repayable finance is an option, how to best use investment, what type of finance to seek, and which fund manager or social bank to work with. Research over the last years, documents that organisations led and/or founded by people experiencing marginalisation face historic and persistent underinvestment and so are disproportionately affected by these challenges.

Activities

Noting the gap in accessible information provision as a significant barrier to investment flowing, alongside sector partners BSC worked with charities and social enterprises to design Good Finance. Its mission is to be the reliable, go-to source of information on all things social investment, enabling charities and social enterprises to navigate social investment, and to unlock their ability to use it when it’s the right tool for the job.

To support minoritised leaders in particular, Good Finance has developed a range of programmes and dedicated support. The Addressing Imbalance programme works closely with partners to reach charities and social enterprises led by people from racialised and marginalised backgrounds, providing tailored information and support, and delivers a range of community events. The Social Investment Unpicked e-learning programme provides bursaries for learners from minoritised backgrounds, and the Investment Committees of the Future programme aims to bring broader lived experiences into decision-making in the sector.

Outputs, outcomes and impact

The Good Finance website has so far had more than more than 592,000 unique users, engaging with a range of interactive tools (such as the “Is it right for us?” diagnostic tool, cost of capital calculator and the outcome matrix), educational content and resources. One in three of these users goes on to visit investor websites through the directory, which has seen more than 189,000 unique users. Good Finance also hosts in-person and online thematic and geographic events, which have supported more than 3,500 people to demystify social investment. More than 200 participants have completed the e-learning programmes.

The Addressing Imbalance Community Event gave me incredible insight into how social investment is understood and worked on at every level – from the entrepreneur to the investor – and how the imbalance/barriers vary at all these different stages.

The Addressing Imbalance Community Event gave me incredible insight into how social investment is understood and worked on at every level – from the entrepreneur to the investor – and how the imbalance/barriers vary at all these different stages.