Market Building and Investing

Delivering on our Theory of Change: BSC’s 2020-25 Strategy

Our 2025 strategy builds upon our Theory of Change and what we have learned in previous years. It focuses on building four market systems where there is greatest potential for scale of impact and where we believe we can make the biggest difference. This section goes into more detail on our market building and investing activities in each of these market systems. It also provides a summary of the progress we have made, and what we have learned in each of the four market systems against the goals and KPIs we set as part of our initial theories of transformations for each market system.

Impact venture

Helping build a venture market that nurtures and scales innovative ways of tackling social problems

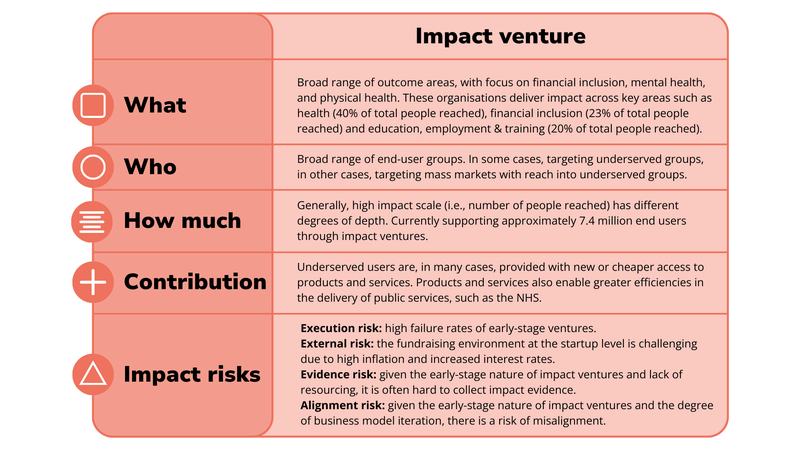

We are building a venture market that nurtures and scales innovative ways of tackling social problems. Tech can drive impact at huge scale, quickly, tackling problems in ways other solutions cannot. We believe that tech-enabled business models have the potential to transform the lives of many people. These organisations deliver impact across key areas such as health, financial inclusion and education, employment & training.

There are various changes that need to happen to realise this opportunity. Many of these involve a change of mindset towards generating meaningful impact alongside strong returns, and impact as driving value is necessary. The practices that sit behind that – developing understanding and implementation of impact practice that is valuable and proportionate. We believe these changes will help to tilt the venture ecosystem towards impact, enabling business model innovation that delivers on the impact potential of ventures.

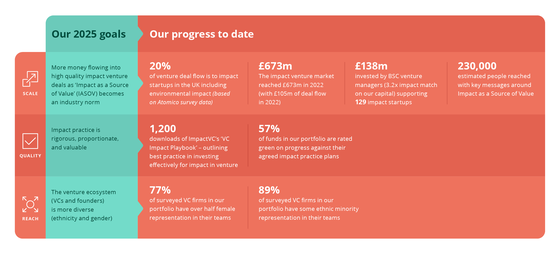

Impact venture highlights

- In 2023 we saw more capital flowing to impact companies and more impact ventures funds being set up. Through our venture managers, we have now invested in more than 100 impact companies, reaching over 7.4 million people in the UK. Three million people have received support to improve their mental or physical health and 1.8 million people have been able to better manage their financial situation through improved access to credit, insurance and flexible pay products.

- There is step change in the way VCs are coming together to accelerate impact. In 2023 we launched the ImpactVC community, to improve connectivity among peers and develop best practices. The community now features more than 750 people from over 570 firms, who collectively manage more than £50 billion of assets.

- We have continued to build the evidence base to demonstrate how impact is driving value, through the publication of five case studies of high-performing impact companies. The increased capital flow through venture funds demonstrates how more investors are seeing that impact can act as a source of value.

Market-building in impact venture

To fully unlock venture capital’s impact potential a number of obstacles need to be addressed. Currently there isn’t sufficient capital flowing into impact-targeting start-ups. This is especially the case for founders that are women, Black, Asian or minority ethnic. Historically there has been an assumption that it isn’t possible to generate meaningful impact and strong financial returns together. In recent years we started to see this perception change, and we believe we have a significant opportunity to accelerate the shift towards impact.

Our market building strategies over the last 12 months have focused on:

Throughout 2023 we continued to build and share evidence on Impact as a Source of Value, reaching over 22,000 readers, through the publication of five case studies of high-performing impact companies. We have continued to share this evidence at in-person events, workshops and through webinar series, including through the ImpactVC platform.

The venture capital industry has failed unacceptably to invest in firms outside London and the South East or in businesses led by women and ethnic minorities[1] Against this backdrop, we aim to use our influence to improve EDI in the impact venture ecosystem. We have continued to survey all our VC managers to understand how diverse their teams are, as well as how diverse their portfolio is, and last year we had a 83% completion rate of the survey. EDI continues to be part of the agenda for our Annual Impact Conversations, and we hosted a session for our fund managers covering common challenges with collecting diversity data. We have fed into various sector initiatives including VentureESG and Diversity VC.

Spotlight: ImpactVC

ImpactVC is a community of VCs accelerating impact within venture, incubated at BSC. Through sharing best practice and resources, it aims to drive venture capital's ability to solve social and environmental challenges including financial exclusion, mental ill health and climate change.

There is increasing interest in impact from VCs, as they see the potential for venture-backed start-ups to make a huge difference to social and environmental issues, while delivering outsized returns. But we believe there are two important gaps. Firstly around connectivity between VCs working on impact, and secondly around impact resources tailored to early-stage venture investment.

To unlock the impact potential of venture capital, and help solve world problems, we need high-quality resources and a community of dedicated VCs.

ImpactVC does this through building a community of leaders within venture capital, including VCs experienced in impact, and top-tier mainstream VCs who are newer to impact. Since launching in February 2023, we now have more than 750 VCs from over 570 firms in the community. The community learns together, shares insights and fosters collaboration to accelerate impact within venture capital. The community also co-develops open-source resources to help venture firms invest effectively for impact – such as the VC Impact Playbook.

Investing in Impact Venture

In 2023, we made three new investments with a value of £13.5 million, including Bethnal Green Ventures Fund II – the fund achieved a first close of £33 million with co-investors including the British Business Bank and M&G. The fund aims to support up to 100 start-ups via BGV’s flagship tech-for-good programme.

Since inception BSC has made:

- 23 venture fund commitments managed by 15 managers

- £126 million capital committed

- Representing 14% of our portfolio

Venture Portfolio – Impact on people highlights

The following table provides an overview of the actual impact that our Impact Venture investment portfolio is currently contributing to.

Eka Ventures

In 2020 BSC invested in Eka Fund I, the largest impact-driven, early-stage, venture capital fund in the UK (£68m), to address the urgent need and opportunity to use the power of science, data and technology to build a better economy.

Eka Ventures shares our belief that purpose-led startups can deliver social change, and is building its firm on the premise that impact and financial return can go hand in hand.

Challenge

Many industries are stuck with business models that limit the potential for addressing negative environmental and social impacts and delivering more positive outcomes for people and planet. For such models, improving environmental or social impact performance comes with a significant increase in cost.

Solution

In 2020 BSC invested in Eka Fund I, the largest impact-driven, early-stage, venture capital fund in the UK (£68m), to address the urgent need and opportunity to use the power of science, data and technology to build a better economy. The fund invests in innovative companies that use technology to deliver high growth and profitability in parallel with delivering societal value with a focus on two areas: preventative healthcare and sustainable consumption.

Impact

To date, Eka has invested in 15 innovative companies. Portfolio companies are providing a range of important products and services, from fair and transparent insurance (Urban Jungle) to support to happier and healthier relationships (Paired), and from more sustainable packaging (Sourceful) to cleaner parcel delivery (Hived).

Frontline example

In 2021, Eka invested in Paired, a mobile app designed to improve relationship health. Relationships are an important contributor to health, but there is little help available to couples and therapy is expensive. Paired offers a range of simple tools to help couples build healthy relationships. Their vision is a fully personalised offering that helps couples navigate major transition points, such as having children.

User voice

Having direct and ongoing access to end-user feedback is important for Eka to understand and support its portfolio companies in the best possible way. To make this possible, Eka is automatically scrubbing end-user reviews on Trustpilot for its portfolio companies and feeding them back into its internal team slack channel on a daily basis.

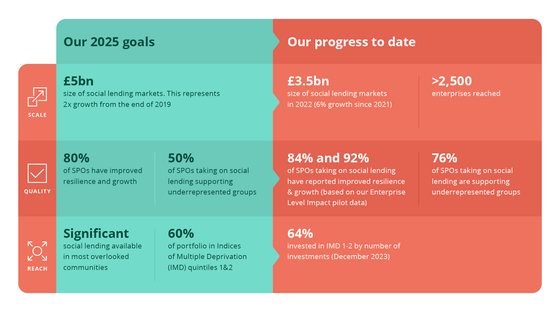

Social lending highlights

- Blended finance – grants, guarantees and tax relief – is a critical bridge between the needs of enterprises and investors in the social lending market, while enabling both grant-makers and investors to achieve greater impact with their capital.

- There has been positive momentum in 2023, with £87.5 million new government commitments of dormant assets, as partners collaborate to build a blended finance market for the long term and create more immediate solutions to the cost-of-living crisis such as the £19 million Energy Resilience Fund.

- Social lending market has a unique ability to reach under-represented people and places, and support those enterprises to become more resilient: 64% of BSC investments are located in the 40% most deprived areas.

Market-building in social lending

In the social lending market, there can be a disconnect between the financing needs or business models of enterprises supporting underserved communities, and the requirements of investors who have the capital needed to grow this market. This creates challenges for the growth and sustainability of the fund managers that are experts in providing finance to enterprises. These challenges are exacerbated by barriers faced by more diverse-led organisations and those operating in areas of higher deprivation. Growth in the market reflects where there is greatest alignment between the needs of enterprises and investors: over a ten-year period, the strongest growth has been in social banks and charity bonds, while development and sustainment of the non-bank lending market have been underpinned by building the blended finance market through Access – The Foundation for Social Investment and others

Our market building strategies over the last 12 months have focused on:

Collaborative policy efforts such as the Community Enterprise Growth Plan have secured additional dormant assets, ensured the government’s Recovery Loan Scheme guarantee works for charities, and improved terms of Community Investment Tax Relief. [These are attracting new institutional investors to enable sectors like CDFIs to scale up – eg CIEF II.]

In 2023 rapidly rising interest rates and severe cost-of-living pressures have placed pressure on some business models’ resilience, while increasing the returns that many investors are looking for and slowing fundraising. Against this backdrop, BII successfully launched Fund IV with new investors into impact such as Beazley and Aspen.

The Addressing Imbalance programme is improving our understanding of the barriers that need to be addressed in partnership with others, to expand the diversity and reach of social lending, with 80 participants in the Investment Committees of the Future Initiative.

Social Investment Business - Recovery Loan Fund

BSC worked with Social Investment Business (SIB) to establish the £25 million Resilience and Recovery Loan Fund during the early stages of the pandemic. This initiative assisted nearly 80 social sector organisations in sustaining their services.

Challenge

As the social sector emerges from Covid-19, charities and social enterprises are facing a new set of challenges. Some have experienced increased demand for their services as a result of the lingering negative social effects of the pandemic and lockdowns and others have had to pivot their business models to cope with the new environment, or refinance borrowing taken on to survive the crisis.

Solution

BSC worked with Social Investment Business (SIB) to establish the £25 million Resilience and Recovery Loan Fund during the early stages of the pandemic. This initiative assisted nearly 80 social sector organisations in sustaining their services. Building on this success, BSC invested in the Recovery Loan Fund (RLF) to ensure continued financial support for these organisations during the recovery phase.

Impact

The RLF, managed by SIB in partnership with several other social lenders, delivers loans backed by the government’s Recovery Loan Scheme to social sector organisations. The wide network of partners ensures that the fund can reach a diverse set of borrowers, while the government guarantee helps keep costs low for borrowers and attracts investors. A grant provided by Access – The Foundation for Social Investment also allows the fund to target Black, Asian and Minoritised Ethnic (BAME[2])-led organisations, and looks to address historical imbalances by offering unrestricted grants, bespoke business support, and reducing eligibility and loan size criteria for the RLF. To date nine out of 33 applications submitted from Black, Asian and Minoritised-Ethnic-led charities and social enterprises have been approved, resulting in £1 million in grants approved.

Frontline example

Contento Social Homes, a Black- and Minoritised Ethnic-led organisation, originally worked with homeless individuals who required refuge and living support. During the pandemic, Contento Social Homes faced a surge in referrals from women seeking refuge from domestic abuse, overwhelming existing capacity within Birmingham centres. The lack of available spaces led to the urgent need for alternative housing solutions.

SIB supported Contento when the opportunity to buy a home came up, with a loan and grant from the RLF. It was also able to purchase a van to transport residents and pay for some vital maintenance.

User voice

SIB prioritises incorporating user input into its decision-making processes. Notably, the Recovery Loan Investment Committee consistently includes either a past customer or a member of the SIB community panel. SIB actively solicits customer feedback during key stages such as funding applications and throughout ongoing relationships, especially when outstanding funding is involved. This qualitative information, coupled with objective data, forms the basis for continuous review and adaptation of funding strategies. An illustrative success of this approach is evident in the case of the RLF, where feedback and data revealed a lack of outreach to BAME-led organisations. In response, SIB introduced the Flexible Finance programme alongside the RLF, significantly increasing investments in such organisations from approximately 4% to around 25%.

Investing in social lending

In 2023, we made five new investments in social lending funds with a total value of £22.6 million. These investments tackle specific missions and are both seeding new investment solutions and scaling more proven strategies, for example:

- Energy Resilience Fund (Key Fund and SIB): Social enterprises, charities and community enterprises are struggling with rising energy bills, yet can lack the finance and expertise for cost-reducing energy efficiency measures. The Energy Resilience Fund will provide blended finance and technical support to help address the vulnerability of SPOs to energy price volatility and strengthen their resilience.

- BII Fund IV: BII has recognised a market gap for medium-sized, asset-backed SPOs in Care, Housing and Social Infrastructure, that are seeking to grow to meet growing social needs. The fund provides unitranche loans, a solution tailored to the needs of organisations that would otherwise be able to access the amounts of finance needed only through complex deals with multiple finance providers.

Since inception BSC has made:

- 56 social lending fund commitments

- £368 million capital committed

- Representing 40% of our portfolio

Social lending portfolio – Impact on people highlights

The following table provides an overview of the actual impact that our social lending investment portfolio is currently contributing to.

Spotlight: Enterprise Level Impact framework

In 2020 BSC worked with several fund managers to co-develop a shared framework, to better understand the effect of investments on the enterprises’ resilience and growth. Identifying the types of organisations using social investment and what they are using he investment for enables us to better target growth and identify gaps in the market.

The dashboard below provides an overview of the reasons why enterprises take on social lending.

Understanding why enterprises take on social lending

Strengthening enterprise resilience and growth continues to form an important part of our investment objectives in this market system. The framework was piloted in 2021/22, and during 2023 we have focused on better understanding why organisations take on social investment, and what they spend the proceeds on.The framework includes data on 501 SPOs across nine fund managers – the project is still in the first year of rollout and the sample sizes are therefore limited. As the framework progresses, the sample size will reflect the social lending sector as a whole.

The key insights from the data collected so far indicate that:

- The most common reason SPOs are taking on social investment, is growth and expansion. Given the quick sequence/subsequence of crises, we would have expected a higher rate of organisations taking on investments to bridge lost income streams or support cost-cutting and consolidation. Instead, many investments were used to enable services and products to be created or expanded. Growth through either new or existing product or service continues to be the top two primary purposes of investment. During the pilot 30% of organisations were accessing social investment to grow through existing product or service; this has now increased to 45%.

- Since the pilot we have seen a higher proportion of SPOs leveraging their social investment to acquire fixed assets (property or land). While supporting ongoing operating expenses and human capital (such as hiring new employees) remains a use of proceeds among the SPOs in the data set.

This content is not visible because you have denied third-party cookies. Update your cookie settings and refresh the page to interact with this element.

Social Outcomes Contracts

Helping build a market that improves the lives of people with complex needs, while creating better value in public service delivery.

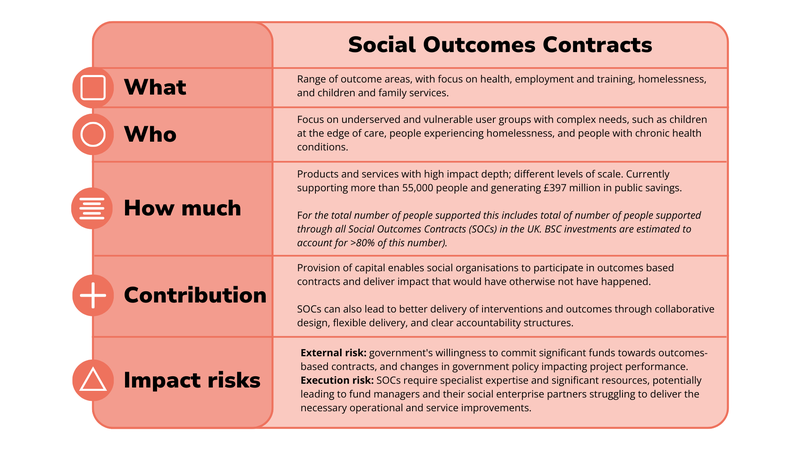

We are building the social outcomes contracts (SOCs) market to create better outcomes for individuals with complex needs, and better value for government in public service delivery. An outcomes-based approach can lead to better flexibility in delivery, more accountability and better collaboration.

Social enterprises and charities often lack the upfront working capital or risk appetite to deliver social outcomes contracts. These organisations need flexible funding to deliver their services, in advance of outcomes payments being made. Capital from socially motivated investors, who are repaid only if outcomes are achieved, can help bridge this gap.

SOCs highlights

- £1.4 billion of public value delivered through social outcomes contracts in the UK, equivalent to £10 for every £1 government spend.

- There is a growing coalition of supporters of SOCs, including NHS Confederation, which helps amplify all voices and leads to enable better traction, with 180 commissioners using outcomes contracts.

- Together, this has resulted in key partners such as His Majesty’s Treasury (HMT) seeing greater opportunities for outcomes commissioning.

Market building in SOCs

Continuing the growth of the market and delivering impact to highly vulnerable individuals hinge on several key factors. Many politicians and civil servants are not aware of what SOCs are or the value they can bring, or were operating under common misapprehensions, such as that SOCs are overly complex or that private investors generate outsize returns from them.

While other barriers do exist, such as ensuring social enterprises and charities understand the value SOCs can provide to them and their beneficiaries, crowding in sufficient levels of investments, and building a fund manager landscape able to absorb that investment, these are all contingent on bringing in additional government support. Many politicians and civil servants are not aware of what SOCs are or the value they can bring, or were operating under common misapprehensions, such as that SOCs are overly complex or that private investors generate outsize returns from them.

Our main strategies therefore focus on this aspect of the system:

We have built significant relationships with key individuals across areas where outcomes partnerships can be most effective. This resulted in a small allocation of £37.5 million in the Spring Budget by Treasury, to fund innovative initiatives to help people into work, but this has yet to translate into actual projects or match the scale of our ambition.

We have continued to create and share content (such as a deep dive on the role SOCs could play tackling complex health issues and key data on public benefit and impact created at system level for government and individuals and have attended (and presented at) key events and roundtables.

We are making progress, especially in the health sector through working with the NHS Confederation. We have also built more significant partnerships with think tanks and other agencies, eg E3M Local Commissioners’ Group, Future Public Services Taskforce with Demos, and others. We see the need to do more to bring in delivery partner and commissioner voice to these coalitions.

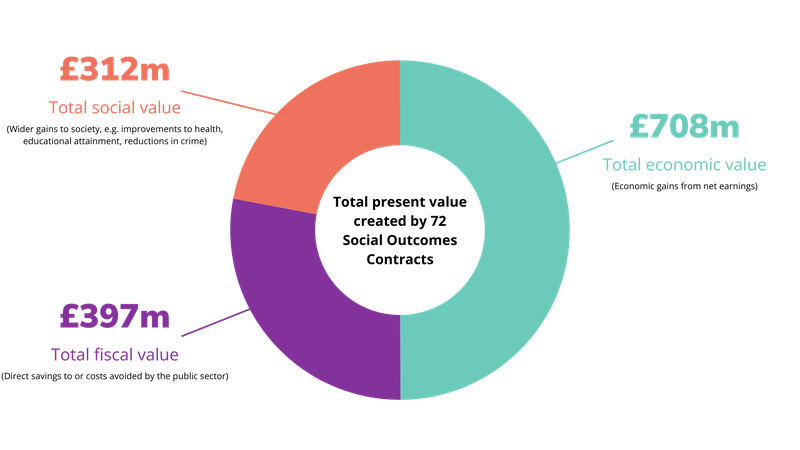

Spotlight: Quantifying the impact of SOCs

Our vision for the SOCs market is based on the belief that SOCs can deliver significant impact and better outcomes for individuals with complex needs, and better value for money for government. We commissioned a report which shows for the first time how over the last decade, the Social Outcomes Contracts market has grown and added significant value to thousands of individuals facing complex social issues.

However, there has never been a comprehensive attempt to quantify the value created by SOCs in the UK. This made it difficult to substantiate our claims in conversations with key stakeholders.

As a result, BSC commissioned an independent study by ATQ Consultants to research this. Its findings 'Outcomes for All report' were published in mid-2022 and were launched at an event in Parliament. We have since been working on repeating this analysis on an annual basis, and on refining and improving the underlying methodology by working with other partners in the SOC market.

The analysis, which was conducted on 72 SOCs out of a total 90 in the UK (for which data was available), showed that over £1.4 billion of public value has been created by outcomes achieved to date, at a cost of just under £140 million to commissioners. That means for every £1 that government has spent, a further £10 of public value has been created, nearly £3 of which is fiscal (cash saved and costs avoided). These findings have been referenced in Parliament and have provided a firm evidential base for our engagement work.

Investing in SOCs

Our most recent investment, made in 2018, was in Bridges Social Outcomes Fund II. This is currently the only SOC fund in the UK that is still actively investing. We have not made any new investments pending further government commitments to outcomes-based contracting.

Since inception BSC has made:

- 13 fund and direct commitments in SOCs

- £44 million capital committed

- Delivering outcomes for at least 45,000 people

- Representing 5% of our portfolio

Social outcome contracts portfolio - Impact on people highlights

The following table provides an overview of the actual impact that our SOCs investment portfolio is currently contributing to:

Bridges Social Outcomes Fund II (SOF2)

The follow-on Bridges Social Outcomes Fund II includes contracts across children’s services, homelessness and health and social care, tackling some of society’s most entrenched issues with a focus on those with the most complex needs.

Challenge

National and local government is effective in delivering large-scale generalist public services. But for complex areas such as homelessness, traditional public service siloes struggle with tailoring long-term support to individual need. The result is that the individual’s problems can persist and worsen, leaving public services to firefight crises rather than prevent them.

Solution

Bridges Fund Management launched its second fund dedicated to social outcomes contracts, building on the learnings from its first Social Impact Bond Fund. The £35 million Bridges Social Outcomes Fund II (SOF2) backs projects commissioned by local and central government departments, as well as other commissioners, across several policy areas. Individuals using services in these areas often interact with multiple parts of the state; so an approach that uses collaborative design, flexible delivery and clear accountability is crucial to the success of these services. Through Bridges Outcomes Partnerships, SOF2 provides upfront working capital and additional capacity-building resource to delivery partners, providing vital local services in areas such as children’s services and child protection, employment, health and social care, education and homelessness.

Impact

Revenue is fully contracted through the life of the contracts and is conditional upon achieving meaningful, pre-agreed, positive milestones – outcomes – without the constraints of detailed specifications or artificial KPIs. It creates better outcomes and better value for money than traditional public service approaches. So far, SOF2 has supported 25,707 people, many highly vulnerable with complex and overlapping needs, across 25 contracts, delivering £76.6m of short-term value to the UK government.

Frontline example

Bridges Outcomes Partnerships supported local authorities and NHS bodies in Northamptonshire to pioneer a new social prescribing programme called SPRING, which works to create sustained lifestyle changes and improved self-care for people living with long-term health conditions such as diabetes, asthma and heart disease. The programme maps existing community assets and works in collaboration with statutory and community organisations to effectively tailor its support to what will make a real difference for each person. “Link workers” across three experienced delivery partners are delivering services to over 1,000 people so far.

User voice

The partnership gathers feedback from frontline staff, so that they can track progress with participants and identify additional areas of support needed to address health concerns. Early on this process found that a high proportion of participants had acute mental health needs. In response the partnership put together a programme of “first aid mental health training” for staff.

Social property

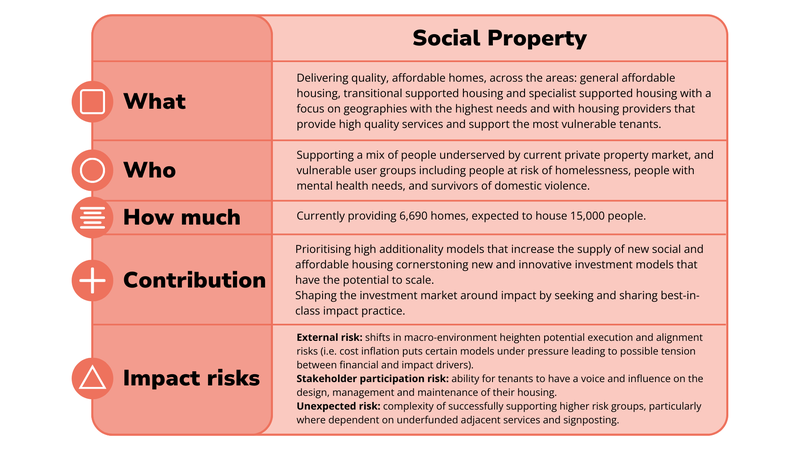

Helping build a housing market ecosystem that creates more safe, secure and affordable homes for everyone to access, regardless of their circumstances, particularly for the most vulnerable people in our communities.

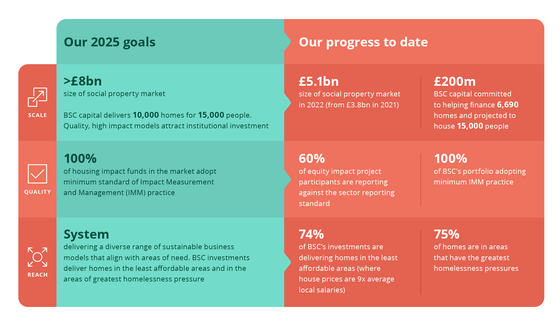

Our goal is to increase the supply of good-quality, social and affordable housing in the UK, particularly for the most vulnerable. The UK has a housing crisis, which is affecting people across the income spectrum, but particularly those who are most vulnerable. Tackling the chronic shortage of social and affordable housing requires an estimated £16.9 billion every year for the next ten years. And government figures show that more than 100,000 households including over 130,000 children are in temporary accommodation, the highest figure since records began. Local authorities are close to bankruptcy as they struggle to house families in need – with councils in England paying £1.7 billion per year for temporary accommodation.

Impact-driven private capital has a vital role to play in increasing the supply of social and affordable homes, and its contribution has been increasing since 2011, growing from virtually zero to £5.1 billion. Private impact capital is actively involved in three primary segments: General Needs Social and Affordable Housing, which supports low-income households in accessing quality, secure and affordable homes; Specialist Supported Housing, addressing the demand for specialised housing for individuals requiring additional support; and Transitional Supported Housing (TSH), ensuring those in crisis and facing homelessness have access to safe and appropriate transitional housing, supporting their transition to stable, independent living.

Social property highlights

- We help institutional investors understand how to invest for impact in social and affordable housing, we engaged with investors with over £500 billion AUM in 2023.

- Despite a changing macroeconomic environment, we saw an additional £140 million from institutional investors into BSC-backed investments, reflecting continuing appetite for the sector from Local Government Pension Schemes targeting levelling-up investments.

- There is growing evidence from our portfolio of how impact investment in social and affordable housing delivers impact in high-need areas, with 75% of investments focused on homelessness delivering homes in areas where the rates of homelessness are at their highest.

Market-building in social property

We have identified several structural factors within the investment ecosystem, that either pose barriers or present opportunities. Firstly, investors perceive the sector as complex and high risk, often stemming from a limited understanding of the underlying business models. Secondly, housing partners, charities and social enterprises are sometimes wary of new forms of private capital entering the market, due to a lack of transparency and consistency in impact practices and measurement across the industry. Lastly, the market’s relatively nascent stage means that a visible track record is not always evident to stakeholders, further influencing perceptions and decisions within the evolving landscape.

Our market building strategies over the last 12 months have focused on:

We engaged with investors with more than £500 billion AUM and industry press to share knowledge on impact business models, risks, mitigants and opportunities. Targeted engagement with Local Government Pension Schemes led to more than £140 million of co-new investments against a challenging macroeconomic backdrop.

In partnership with DLUHC and Manchester Metropolitan University, we launched a longitudinal study on homelessness investment, while our review of the Equity Impact Project highlighted an opportunity for ongoing sector utility.

Increased public affairs engagement, including providing expertise and evidence to a Parliamentary Select Committee (The finances and sustainability of the social housing sector – oral evidence). This builds on our experience of delivering for and with government: £25 million of catalytic capital from DLUHC to help scale the homelessness impact models, which has levered in a further £123 million of private investment.

Spotlight: Property portfolio analysis

We carried out some analysis to better understand how our property investment portfolio is performing against its strategic impact objectives of addressing the structural under supply of affordable housing and providing homes for those in greatest need.

The deep dive brings together a detailed dataset of underlying property information BSC has been collecting across the portfolio alongside external, national and local data sources. This includes data from investments in 16 funds, financing nearly 6,690 homes, which will house over 15,000 of the hardest-pressed people in the UK.

Addressing the structural undersupply: BSC has funded the supply of 4,577 General Needs Affordable homes in the UK, of which 87% are affordable, and 61% are the most affordable tenures (social and affordable rent); 74% of the General Needs Portfolio is in areas of “constrained affordability”[3].

Homes for those in greatest need: Three quarters of the TSH Portfolio is in areas where the incidence of homelessness is above the national average, and 65% of TSH delivery in areas with the highest homelessness pressures, helping tackle the nearly 100,000 households spending each night in temporary accommodation in the UK.

Investing in Social property

In 2023 we made two investments in social property with a value of £16.75 million, focused on scaling up innovative high-impact models in Transitional Supported Housing (TSH), while also developing new funds that will attract institutional capital:

- Social and Sustainable Housing II: The housing market in the UK does not provide safe and affordable housing for vulnerable people in the quantity or quality they require. Some charities face considerable hurdles, such as cash shortage, when attempting to purchase or acquire additional properties. BSC invested £6.75m as a follow-on investment into SASC’s second property fund, which aims to support the scaling of a high-impact business model with charities.

- Octopus Affordable Housing Fund: A social housing shortfall is resulting in 130,000 children living in temporary accommodation in England. Meanwhile, building new homes has become increasingly challenging, due to rising costs and a housing association sector under pressure to focus its resources on improving existing stock. BSC has invested £10m into the fund, which will target long-term strategic equity partnerships with housing associations, to deliver affordable and energy-efficient housing for low-income households.

Since inception, BSC has made:

- 20 fund commitments in social property

- £237 million capital committed

- 6,690 homes to be delivered across the UK

- Representing 25% of our portfolio

Social property portfolio – Impact on people highlights

The following table provides an overview of the actual impact that our Social Property investment portfolio is currently contributing to.

Social and Sustainable Capital (SASC) – Social and Sustainable Housing (SASH) Fund

The SASH Fund provides finance for social enterprises and charities with a track record of both delivering support and managing property. It generates positive social outcomes by providing support services to vulnerable people such as those fleeing domestic abuse, children leaving care or ex-offenders.

Challenge

At least 200,000 people in the UK live in supported housing. Government figures show that more than 100,000 households, including over 130,000 children, are in temporary accommodation, the highest figure since records began. Many small and medium-sized charities that provide accommodation-based support services struggle to access safe, stable and appropriate housing. This restricts their potential to support disadvantaged individuals and families.

Solution

The Sustainable and Sustainable Housing (SASH) Fund – which was developed by SASC in partnership with social enterprise and charity partners – provides lending to charities to purchase safe, affordable accommodation for the people they support.

Impact

SASH I has enabled 20 charities to purchase 445 properties, which are supporting 717 tenants. Tenants are very often those excluded from the mainstream housing market – including those experiencing challenges such as domestic abuse, homelessness or living with disabilities.

Frontline example

Thrive Women’s Aid is a charity that supports women and their children affected by domestic abuse in Neath Port Talbot. Neath Port Talbot faces significant challenges, with elevated levels of deprivation, poverty and disadvantage. Within the county borough, 14 areas rank among the top 10% of the most deprived communities in Wales. The pandemic exacerbated these issues, leading to a 42% surge in referrals for the charity’s adult services.

Thrive Women’s Aid received a loan from the fund to purchase 20 properties in the Neath Port Talbot region, which will serve as safe move-on accommodation, where support services can also be delivered to help women and children rebuild their lives.

User voice

SASC Investment Committee includes two members who are both former CEOs of social sector organisations and bring invaluable insights into beneficiary needs or experiences. As part of their due diligence on a given charity, SASC will conduct first-hand research by speaking to staff, local authority commissioners, charity peers, etc.

Social lending

Helping build a social lending market that meets the needs of a diverse range of social purpose organisations and investors alike.

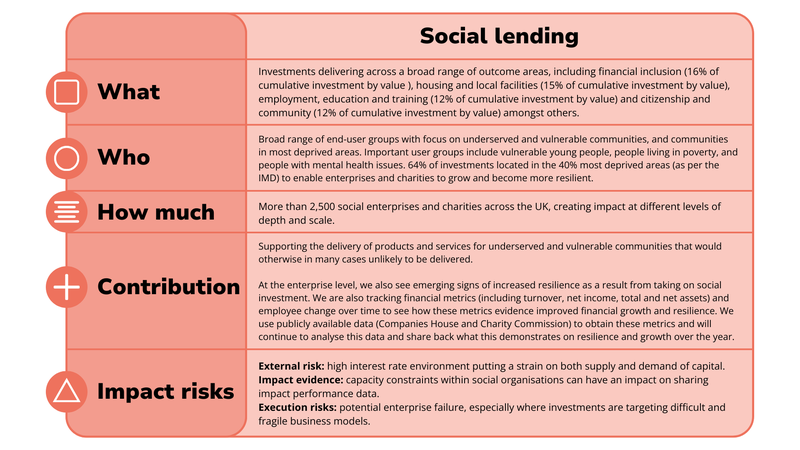

We are building thriving social lending markets where investors can find opportunities that align with their values, and social purpose organisations can find the right finance at the right time to fuel their work improving people’s lives across the UK. These organisations deliver impact across key social issues such as financial inclusion , housing and local facilities and employment, education and training and are addressing critical societal challenges such as the Just Transition.

The social lending market system provides a range of lending products to social purpose organisations (SPOs), spanning small loans, charity bonds and social bank loans. Many of these enterprises work in some of the most disadvantaged communities across the UK and, with the right type of finance from mission-aligned lenders, can grow their impact and organisational resilience.