Values alignment

There are numerous examples where having a negative impact has resulted in businesses shedding customers. More than half of Volkswagen customers said that they were put off from re-buying a car following their carbon emissions scandal. This exemplifies a growing trend where consumers are increasingly focusing on impact-related factors when making purchasing decisions. Therefore, companies with a higher impact focus should acquire and retain more customers compared to impact agnostic companies.

This is quite hard to isolate and test given often many things vary between two companies. One data point comes from a comparison of Uber and Lyft. Whilst these are not ‘deep impact’ examples (there is limited data here), it highlights how very similar organisations with different impact intent can have very different outcomes. The two ride hailing businesses have very similar business models, price points and technology. However, Lyft boasts a superior customer retention rate at 18% compared to Uber’s 10%. While there are differences between the two which might drive this (no pun intended), one standout difference is their approach to impact and Environmental, Social and Governance (ESG). According to this research brief from Truevalue Labs, Lyft has had superior performance on ESG, particularly in areas of social and human capital issues which we believe is leading to higher customer retention through greater values alignment. Having a closer look at why customers choose Lyft supports this idea. For example, many were a fan of the ability to tip drivers. Uber took longer to introduce this feature.

While value alignment might play a role, it’s also plausible that a greater focus on impact at Lyft results in an improved customer experience. Many of their impact initiatives directly affect the end user. For example, Lyft provides better working conditions to drivers , which results in higher driver satisfaction which in turn could result in a higher proportion of satisfied customers. This brings us to the second pathway to higher retention:

Impact-driven innovation results in better products

Startups disrupting the short-term financing sector, serving people on low incomes, is a great example of how impact drives innovation and supports customer retention. Historically, this sector was dominated by payday lenders charging extortionate interest rates to lend to people on low incomes who have few alternative sources of finance. Wonga, the most high-profile example of this in the UK, was charging 5,853% APR to its customers, claiming high interest rates were needed to offset defaults across their loan book to this perceived risky group of borrowers. This was hugely detrimental from an impact perspective, with customers often forced into a repeat cycle of borrowing to service the interest on their borrowing.

Driven by a desire to address the social issue, an innovative business model has recently emerged: salary finance. Here, organisations mitigate risk by leveraging earnt but unpaid wages to advance customers’ cash. Therefore, there is no need to offer loans at extortionate rates. These salary finance startups offer financing at a tenth of the price of the cheapest alternatives. This impact-driven innovation results in substantial cost savings and high customer satisfaction leading to retention rates which exceed those of payday lenders despite removing the debt traps. The handful of startups in our portfolio using this model have Net Promoter Scores in the 50s and exceptional customer retention rates of more than 90% compared to ~80% estimated for payday lenders.

This example also demonstrates the added value of being proactively focussed on contributing to a solution that solves a social problem going beyond being merely aligned with customer values as in the ride hailing examples above.

Reaching underserved groups

Impact startups often strive to help underserved groups of society as part of their mission. These groups often experience worse outcomes because of poorly designed or inaccessible products. Meeting these groups’ needs results in increased customer retention through two pathways.

First, underserved customers have few (if any) choices and retention is therefore by default very high. For example, Lemonade, an affordable insurance provider and certified B-Corp, states 87% of its customer base are first time insurance buyers. At an average age of 30 years old, Lemonade has found a way to appeal to a traditionally underserved market segment. Given the lack of competition (indicated by the low insurance take up rate), it stands to reason that Lemonade should experience a higher retention rate. There is some evidence of this. Average retention rates in home insurance are around 60-65%, and yet, despite serving a difficult customer group, Lemonade’s retention rates have been growing steadily to 81% in the first quarter of 2021.

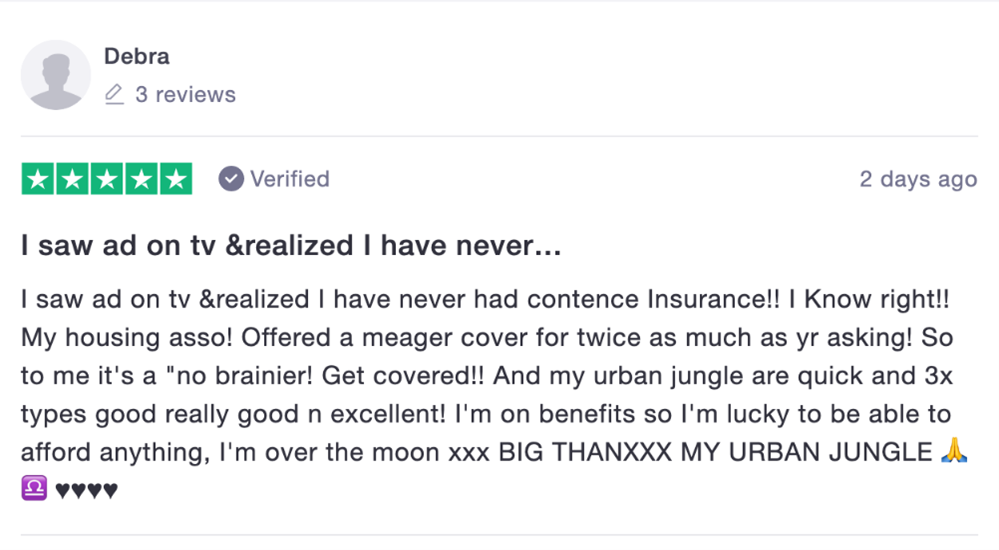

The second driver of retention here is the goodwill that is built by being the first company to solve a painful problem for end users. Sticking with affordable insurance, this is a review from UK based insurer Urban Jungle:

It’s easy to imagine a customer with an experience such as this being more likely to stick with a provider compared to a customer that has lots of existing options. Therefore, we expect that impact-driven startups targeting underserved groups should, all else being equal, see higher retention rates than their counterparts not targeting underserved groups.

In summary…

We believe that taking an impact lens to strategic decision making and product design can help drive customer retention through creating values alignment with customers, driving better products and reaching underserved groups.

While we recognise these are only a few datapoints, we are hopeful that this is early evidence of increasingly important connections between impact and value. In future blogs we’ll continue to articulate how impact can be a source of value and bring in other perspectives from our portfolio and beyond.